文章目录

- 分析目的

- 一、数据采集

- 1、数据来源

- 2、数据说明

- 二、数据传输

- 三、数据处理

- 1、查看数据

- 2、清理无用特征值

- 3、标签列分析

- 4、清理只单一值的列

- 5、空值处理

- 6、数据类型转换

- 四、数据挖掘

- 1、构建模型

- 2、导入算法

- 五、总结

分析目的

本文针对某信贷网站提供的2007-2011年贷款申请人的各项评估指标,建立关于信贷审批达到利润最大化模型,即对贷款人借贷状态(全额借贷、不予借贷)进行分类,从而实现贷款利润最大化,并采用不同算法进行评估。

一、数据采集

1、数据来源

数据来源,这个要注册登录,也可以直接点击下载数据链接下载。下载链接,提取码:nkvk

2、数据说明

本数据集共有四万多头数据,包含52个特征值,其中数据类型分别是 float64型30个, object型22个。本次数据分析主要是实现贷款利润最大化,所以不需这么多特征量,需要对其进行舍弃处理。

二、数据传输

将数据导入到PYTHON软件:

import pandas as pd

loans = pd.read_csv('LoanStats3a.csv', skiprows=1)

half_count = len(loans) / 2

loans = loans.dropna(thresh=half_count, axis=1)

loans = loans.drop(['desc', 'url'],axis=1)

loans.to_csv('loans_2007.csv', index=False)

loans = pd.read_csv("loans_2007.csv")

loans.info()三、数据处理

1、查看数据

#loans.iloc[0]

loans.head(1)

2、清理无用特征值

了解各数据特征在业务中的含义。观察数据特征,主要清理与业务相关性不大的内容,重复特征值(等级下的另一个等级)以及预测后的特征值(批出的额度),此处的相关性大小凭业务知识进行粗略判断,如申请人的id,member_id,url,公司名emp_title等。

loans = loans.drop(["id", "member_id", "funded_amnt", "funded_amnt_inv", "grade", "sub_grade", "emp_title", "issue_d"], axis=1)

loans = loans.drop(["zip_code", "out_prncp", "out_prncp_inv", "total_pymnt", "total_pymnt_inv", "total_rec_prncp"], axis=1)

loans = loans.drop(["total_rec_int", "total_rec_late_fee", "recoveries", "collection_recovery_fee", "last_pymnt_d", "last_pymnt_amnt"], axis=1)

loans.head(1)

删除无关字段后,剩余32个字段

3、标签列分析

#统计不同还款状态对应的样本数量——标签类分析

loans['loan_status'].value_counts()

统计结果显示,共有9种借贷状态,其中我们仅分析"Fully Paid"(全额借款)和"Charged Off"(不借款)这两种状态。“Fully paid”和“Charged Off”(其他取值样本较少,是否贷款含义不明,直接舍弃),表示同意贷款和不同意贷款,将此特征作为及其学习的标签列,由于sklearn中各及其学习模型值接受数值类型的数据类型,所以我们将“loan_status”映射为数值类型。

将“loan_status”映射为数值类型:

loans = loans[(loans['loan_status'] == "Fully Paid") | (loans['loan_status'] == "Charged Off")]

status_replace = {"loan_status" : {"Fully Paid": 1,"Charged Off": 0,}

}

loans= loans.replace(status_replace)

loans.loan_status4、清理只单一值的列

在进行数据分析时,部分字段对应的值只有一个,应删除这些无关字段

#查找只包含一个惟一值的列并删除

orig_columns = loans.columns

drop_columns = []

for col in orig_columns:col_series = loans[col].dropna().unique()#如果字段值都一样,删除该字段if len(col_series) == 1:drop_columns.append(col)

loans= loans.drop(drop_columns, axis=1)

print(drop_columns)

#将清洗后数据存入一个新的文件中

loans.to_csv('filtered_loans_2007.csv', index=False)

5、空值处理

本文的处理原则是:对于某一特征,如果出现空值的样本较少,则删除在此特征商为空值的样本;如果去空值的样本数量较多,则选择删除该特征。有上述原则知,我们需要对各特征出现空值的数量进行统计。

loans = pd.read_csv('filtered_loans_2007.csv')

null_counts = loans.isnull().sum()

null_counts

发现有四个特征有取空值的情况,其中三个空值数量较少,我们删除对应的样本,另外一个特征“pub_rec_bankruptcies”,空值数量较多,我们删除该特征。

loans = loans.drop("pub_rec_bankruptcies", axis=1)

loans = loans.dropna(axis=0)6、数据类型转换

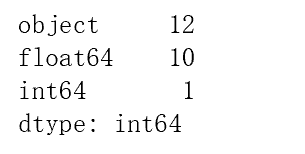

#统计不同数据类型下的字段总和

print(loans.dtypes.value_counts())输出结果如下图,12个列所对应的数据类型为字符型,应转化为数值型。

#输出数据类型为字符型的字段

object_columns_df = loans.select_dtypes(include=["object"])

print(object_columns_df.iloc[0])

#对字符型数据进行分组计数

cols = ['home_ownership', 'verification_status', 'emp_length', 'term', 'addr_state']

for c in cols:print(loans[c].value_counts())

print(loans["purpose"].value_counts())

print(loans["title"].value_counts())

“emp_length”可以直接映射为数值型 ,对于“int_rate”,“revol_util”可以去掉百分号,然后转换为数值型,对于含义重复的特征,如“purpose”和“title”,都表示贷款意图,可选择删除一个,其他与模型训练无关的特征选择删除。剩余的其他字符型特征,此处选择使用pandas的get_dummies()函数,直接映射为数值型。

#将"emp_length"字段转化为字符型数据

mapping_dict = {"emp_length": {"10+ years": 10,"9 years": 9,"8 years": 8,"7 years": 7,"6 years": 6,"5 years": 5,"4 years": 4,"3 years": 3,"2 years": 2,"1 year": 1,"< 1 year": 0,"n/a": 0}

}

loans = loans.drop(["last_credit_pull_d", "earliest_cr_line", "addr_state", "title"], axis=1)

#将百分比类型转化为浮点型(小数类型)

loans["int_rate"] = loans["int_rate"].str.rstrip("%").astype("float")

loans["revol_util"] = loans["revol_util"].str.rstrip("%").astype("float")

loans = loans.replace(mapping_dict)

cat_columns = ["home_ownership", "verification_status", "emp_length", "purpose", "term"]

dummy_df = pd.get_dummies(loans[cat_columns])

loans = pd.concat([loans, dummy_df], axis=1)

loans = loans.drop(cat_columns, axis=1)

loans = loans.drop("pymnt_plan", axis=1)

loans.to_csv('cleaned_loans2007.csv', index=False)

import pandas as pd

#读取最终清洗的数据

loans = pd.read_csv("cleaned_loans2007.csv")

print(loans.info())

四、数据挖掘

1、构建模型

对于二分类问题,一般情况下,首选逻辑回归,这里我们引用sklearn库。首先定义模型效果的评判标准。根据贷款行业的实际情况,为了实现利润最大化,我们不仅要求模型预测正确率较高,同时还要尽可能的让错误率较低,这里采用两个指标tpr和fpr。同时该模型采用交叉验证(KFold,分组数采用默认的最好的分组方式)进行学习。为了比较不同模型的训练效果,建立三个模型。

2、导入算法

初始化处理

#负例预测为正例

fp_filter = (predictions == 1) & (loans["loan_status"] == 0)

fp = len(predictions[fp_filter])

# 正例预测为正例

tp_filter = (predictions == 1) & (loans["loan_status"] == 1)

tp = len(predictions[tp_filter])

# 负例预测为正例

fn_filter = (predictions == 0) & (loans["loan_status"] == 1)

fn = len(predictions[fn_filter])

# 负例预测为负例

tn_filter = (predictions == 0) & (loans["loan_status"] == 0)

tn = len(predictions[tn_filter])逻辑回归:

from sklearn.linear_model import LogisticRegression

lr = LogisticRegression()

cols = loans.columns

train_cols = cols.drop("loan_status")

features = loans[train_cols]

target = loans["loan_status"]

lr.fit(features, target)

predictions = lr.predict(features)from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import KFold

from sklearn.model_selection import train_test_split

lr = LogisticRegression()

kf = KFold(features.shape[0], random_state=1)

predictions = cross_val_predict(lr, features, target, cv=kf)

predictions = pd.Series(predictions)

# False positives.

fp_filter = (predictions == 1) & (loans["loan_status"] == 0)

fp = len(predictions[fp_filter])

# True positives.

tp_filter = (predictions == 1) & (loans["loan_status"] == 1)

tp = len(predictions[tp_filter])

# False negatives.

fn_filter = (predictions == 0) & (loans["loan_status"] == 1)

fn = len(predictions[fn_filter])

# True negatives

tn_filter = (predictions == 0) & (loans["loan_status"] == 0)

tn = len(predictions[tn_filter])

# Rates

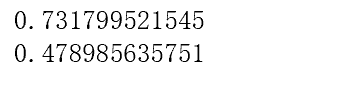

tpr = tp / float((tp + fn))

fpr = fp / float((fp + tn))

print(tpr)

print(fpr)

print predictions[:20]

错误率和正确率都达到99.9%,错误率太高,通过观察预测结果发现,模型几乎将所有的样本都判断为正例,通过对原始数据的了解,分析造成该现象的原因是由于政府样本数量相差太大,即样本不均衡造成模型对正例样本有所偏重,大家可以通过下采样或上采用对数据进行处理,这里采用对样本添加权重值的方式进行调整。

逻辑回归balanced处理不均衡:

from sklearn.linear_model import LogisticRegression

from sklearn.cross_validation import cross_val_predict

lr = LogisticRegression(class_weight="balanced")

kf = KFold(features.shape[0], random_state=1)

predictions = cross_val_predict(lr, features, target, cv=kf)

predictions = pd.Series(predictions)

# False positives.

fp_filter = (predictions == 1) & (loans["loan_status"] == 0)

fp = len(predictions[fp_filter])

# True positives.

tp_filter = (predictions == 1) & (loans["loan_status"] == 1)

tp = len(predictions[tp_filter])

# False negatives.

fn_filter = (predictions == 0) & (loans["loan_status"] == 1)

fn = len(predictions[fn_filter])

# True negatives

tn_filter = (predictions == 0) & (loans["loan_status"] == 0)

tn = len(predictions[tn_filter])

# Rates

tpr = tp / float((tp + fn))

fpr = fp / float((fp + tn))

print(tpr)

print(fpr)

print predictions[:20]

新的结果降低了错误率约为40%,但正确率也下降约为65%,因此有必要再次尝试,可以采取自定义权重值的方式。

逻辑回归penalty处理不均衡:

from sklearn.linear_model import LogisticRegression

from sklearn.cross_validation import cross_val_predict

penalty = {0: 5,1: 1}

lr = LogisticRegression(class_weight=penalty)

kf = KFold(features.shape[0], random_state=1)

predictions = cross_val_predict(lr, features, target, cv=kf)

predictions = pd.Series(predictions)

# False positives.

fp_filter = (predictions == 1) & (loans["loan_status"] == 0)

fp = len(predictions[fp_filter])

# True positives.

tp_filter = (predictions == 1) & (loans["loan_status"] == 1)

tp = len(predictions[tp_filter])

# False negatives.

fn_filter = (predictions == 0) & (loans["loan_status"] == 1)

fn = len(predictions[fn_filter])

# True negatives

tn_filter = (predictions == 0) & (loans["loan_status"] == 0)

tn = len(predictions[tn_filter])

# Rates

tpr = tp / float((tp + fn))

fpr = fp / float((fp + tn))

print(tpr)

print(fpr)

新的结果错误率约为47%,正确率约为73%,可根据需要继续调整,但调整策略并不限于样本权重值这一种,下面使用随机森林建立模型。

随机森林balanced处理不均衡:

from sklearn.ensemble import RandomForestClassifier

from sklearn.cross_validation import cross_val_predict

rf = RandomForestClassifier(n_estimators=10,class_weight="balanced", random_state=1)

#print help(RandomForestClassifier)

kf = KFold(features.shape[0], random_state=1)

predictions = cross_val_predict(rf, features, target, cv=kf)

predictions = pd.Series(predictions)

# False positives.

fp_filter = (predictions == 1) & (loans["loan_status"] == 0)

fp = len(predictions[fp_filter])

# True positives.

tp_filter = (predictions == 1) & (loans["loan_status"] == 1)

tp = len(predictions[tp_filter])

# False negatives.

fn_filter = (predictions == 0) & (loans["loan_status"] == 1)

fn = len(predictions[fn_filter])

# True negatives

tn_filter = (predictions == 0) & (loans["loan_status"] == 0)

tn = len(predictions[tn_filter])

# Rates

tpr = tp / float((tp + fn))

fpr = fp / float((fp + tn))

print(tpr)

print(fpr)

在这里错误率约为97%,正确率约为94%,错误率太高,同时可得到本次分析随机森林模型效果劣于逻辑回归模型的效果

五、总结

当模型效果不理想时,可以考虑的调整策略:

1.调节正负样本的权重参数。

2.更换模型算法。

3.同时几个使用模型进行预测,然后取去测的最终结果。

4.使用原数据,生成新特征。

5.调整模型参数。

)

)

about Humble Numbers)

)